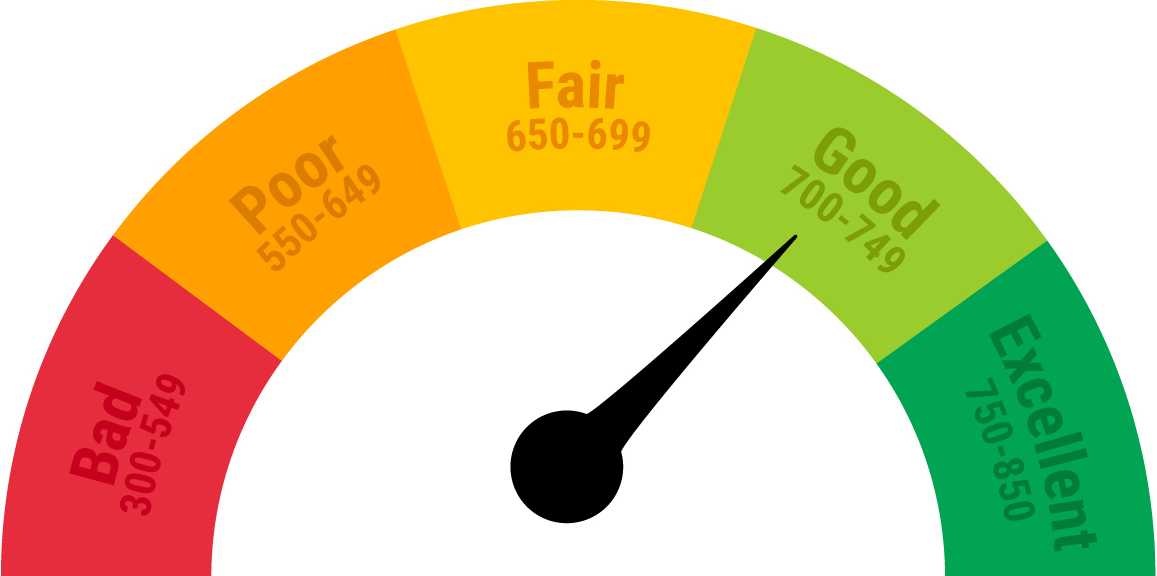

Your interest rate is typically the product of three major factors: the base rate, the lender’s individual policies and your own credit history. The base rate is set by economic market factors, including the Federal Reserve’s current requirements. Lending policies for consumer interest rates may impact the overall cost of the loan. Most of these factors regarding the terms of the loan are out of your control. However, the most important factor in the stipulations of your loan is your credit score because that IS in your control. Your credit score is a numbered value on your reliability on paying debts owed and day-to-day bills. Good and excellent credit scores tend to get you the best APR offers. Fair credit scores get average offers while poor or bad credit ratings may mean you face high interest rates or can’t get approved for a loan at all. Mortgage APRs include fees such as loan origination fees, taxes and private mortgage insurance (determined by the type of loan or if an insufficient down payment is applied). You can add these fees on to the total amount loan, which will be factored into your monthly payment, or you can pay them separately. If the fees are equated into the loan, it will increase the total amount of money borrowed, thus increasing the APR.

Having a close relationship with your Realtor®️ and loan officer who will discuss and explain these terms with you is very important. Finally, the total cost of a mortgage loan also depends on other factors, including how long you finance the property for the overall term of the loan. The longer the term of the loan, the more you will pay over time if all other factors remain the same. On the other side, the shorter the term of the loan, the lower the interest rate you can receive. This will equate to higher monthly payments but a lower total cost. With that being said, a higher interest rate can increase the amount you pay for your home. This is true even if it's over the same time period. A single point in interest can add tens of thousands of dollars in total cost for your home, which is why many people refinance, like we are experiencing now. Also, these point differentials can be major decision makers for consumers to make when deciding on a mortgage. Breaking down percentage points in interest can equate to, depending on the total amount borrowed, saving a couple hundred dollars on your monthly payment. This money saved can be important for reinvesting overall personal capital and wealth.